A cornucopia of news, opinion, views, facts and quirky bits that need to be talked about. Join our community and join in the conversation on all matters aviation. The blog includes our weekly round-up of the bits of European aviation you may otherwise have missed – That Was The Week That Was

Search

Categories

Month of Issue

The privatisation of airports is not a reason for airlines to panic…yet

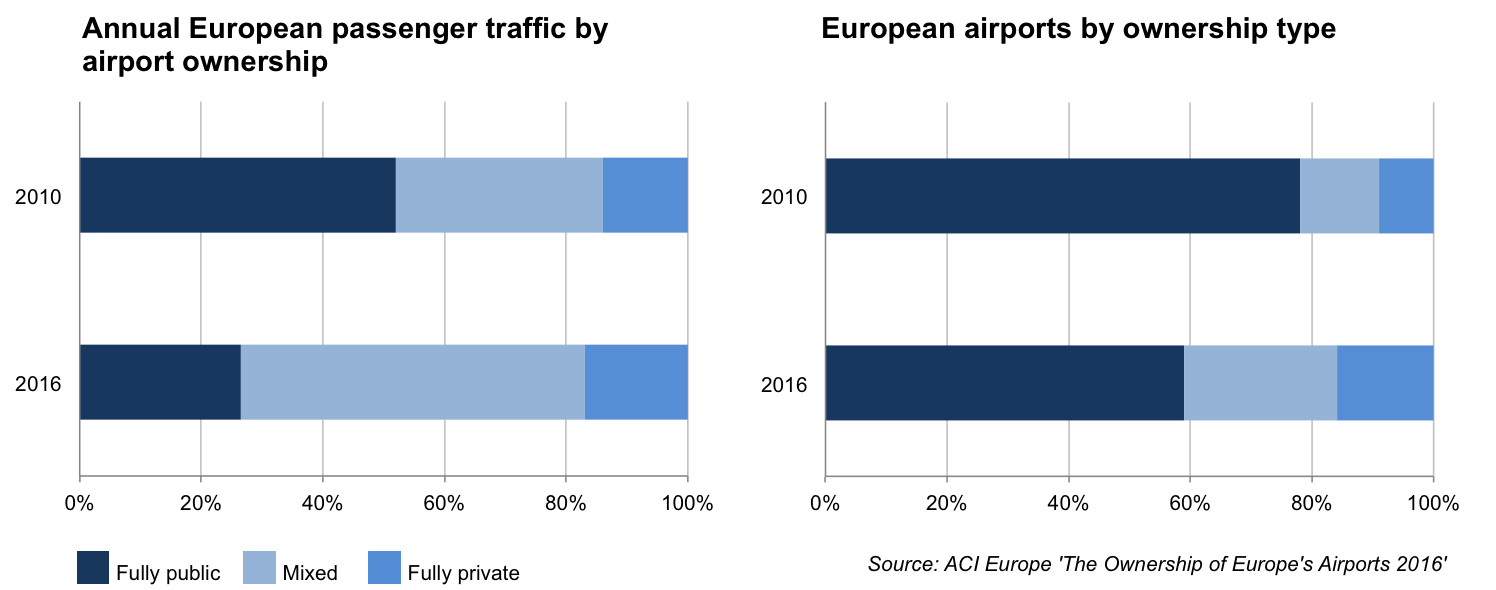

A recent report from Airports Council International (ACI) Europe reveals an interesting statistic: the vast majority of air passengers in Europe (almost 74%) are now travelling through airports that are, to some extent, privately owned. This is up from 48% in 2010. Private ownership is however clearly concentrated in the larger, and more lucrative, airports.

The figures below show the extent of private ownership of European airports in 2016 relative to 2010. In total, 41% of European airports are either privately owned or in joint public-private ownership, almost doubling from 22% in 2010. More privatisation is inevitable, with changes in the ownership of a number of French and Greek airports already in the works.

The ACI report offers up some reasons for this change in ownership. This includes the sale of airports to reduce pressure on public funds and a desire to increase efficiencies and expertise in the running of the airport. (We wonder whether similar pressures could soon be appearing in the air navigation service provider sector). For the ACI, the increasing privatisation of airports is purely a good news story, with upsides for everyone. It is also keen to attribute this trend to commercial pressures arising from increasing airport competition. Well they would, wouldn’t they?

There will be some worried airlines reading the report. After all, private investors will expect a decent return for their investment, and the increasing privatisation of the European airport industry is an indication that airports are providing a lucrative investment. Insert references to monopoly service providers here. Indeed, a report issued by A4E at the start of this year alleges that airport charges have increased by 80% at Europe’s largest 21 airports since 2005.

Before the airlines start banging at the doors of the European Commission demanding heavy-handed regulation (oops – too late), it is worth taking a step back and considering the consequences of the privatisation of European airports.

The first thing to consider is whether privatisation will have any impact on the extent to which there is competition between airports in Europe. Deducing this is no easy task. Both airlines and airports have entrenched views that are not always helpful when it comes to having a real discussion of the issues, while it can be a complex process to measure the ability of passengers and airlines to substitute between different airports.

It is worth considering that the relentless pursuit of profit associated with a private investment has the potential to encourage airports to adopt more innovative approaches to attracting passengers and airlines. In the case of some, this may include attracting customers away from other airports in the region.

Where there is evidence that an airport has market power, this does necessarily mean that its charges are too high or that there is a need for heavy-handed regulation. This applies even with a profit-motivated privatised airport. It is not market power that is the issue, it is the abuse of the market power.

As we discussed in a previous blog post, it may be in the airport’s commercial interests to set aeronautical charges at a level that makes it more attractive to airlines and increase the number of passengers using its facilities. Setting prescriptive pricing guidelines could stifle innovative pricing to the detriment of airlines, airports and ultimately passengers. Privatised airports, with their commercial focus, should be encouraged to challenge the traditional airport business model not buckle under it.

Meanwhile, much of the recent evidence suggests that light-handed regulation can act as a sufficient deterrent, particularly at airports with a strong commercial focus. The threat of further heavy-handed regulation can be enough to incentivise airports to behave in a way that does not antagonise the airlines, and therefore the regulator. After all, being subject to a price or revenue cap can take up a chunk of an airport’s (and an airline’s) resources and limits the airport’s ability to make commercial decisions. Airport regulators in the UK, Australia and New Zealand have all moved towards more light-handed regulatory approaches that, on the whole, have provided to be successful

Increasing privatisation may actually make the economic regulation of airports a simpler task. Many of the traditional tools of economic regulation are designed taking into account the incentives of profit-maximising monopolies. This means they are likely to be most effective when applied to privately owned airports. This sort of regulation may actually have an adverse effect where the airport is under public ownership, where the incentives are less obvious and where the focus may be on the wider benefits of the airport’s operations than purely on financial return.

Of course, increasing privatisation may also mean more airports than before have an incentive to exploit any market power they have in order to increase their profits. The Commission’s decision to review the Airport Charges Directive in 2016-17 is therefore timely. In the meantime, airlines should refrain from pressing the panic button, at least for now.

The ACI report offers up some reasons for this change in ownership. This includes the sale of airports to reduce pressure on public funds and a desire to increase efficiencies and expertise in the running of the airport. (We wonder whether similar pressures could soon be appearing in the air navigation service provider sector). For the ACI, the increasing privatisation of airports is purely a good news story, with upsides for everyone. It is also keen to attribute this trend to commercial pressures arising from increasing airport competition. Well they would, wouldn’t they?

There will be some worried airlines reading the report. After all, private investors will expect a decent return for their investment, and the increasing privatisation of the European airport industry is an indication that airports are providing a lucrative investment. Insert references to monopoly service providers here. Indeed, a report issued by A4E at the start of this year alleges that airport charges have increased by 80% at Europe’s largest 21 airports since 2005.

Before the airlines start banging at the doors of the European Commission demanding heavy-handed regulation (oops – too late), it is worth taking a step back and considering the consequences of the privatisation of European airports.

The first thing to consider is whether privatisation will have any impact on the extent to which there is competition between airports in Europe. Deducing this is no easy task. Both airlines and airports have entrenched views that are not always helpful when it comes to having a real discussion of the issues, while it can be a complex process to measure the ability of passengers and airlines to substitute between different airports.

It is worth considering that the relentless pursuit of profit associated with a private investment has the potential to encourage airports to adopt more innovative approaches to attracting passengers and airlines. In the case of some, this may include attracting customers away from other airports in the region.

Where there is evidence that an airport has market power, this does necessarily mean that its charges are too high or that there is a need for heavy-handed regulation. This applies even with a profit-motivated privatised airport. It is not market power that is the issue, it is the abuse of the market power.

As we discussed in a previous blog post, it may be in the airport’s commercial interests to set aeronautical charges at a level that makes it more attractive to airlines and increase the number of passengers using its facilities. Setting prescriptive pricing guidelines could stifle innovative pricing to the detriment of airlines, airports and ultimately passengers. Privatised airports, with their commercial focus, should be encouraged to challenge the traditional airport business model not buckle under it.

Meanwhile, much of the recent evidence suggests that light-handed regulation can act as a sufficient deterrent, particularly at airports with a strong commercial focus. The threat of further heavy-handed regulation can be enough to incentivise airports to behave in a way that does not antagonise the airlines, and therefore the regulator. After all, being subject to a price or revenue cap can take up a chunk of an airport’s (and an airline’s) resources and limits the airport’s ability to make commercial decisions. Airport regulators in the UK, Australia and New Zealand have all moved towards more light-handed regulatory approaches that, on the whole, have provided to be successful

Increasing privatisation may actually make the economic regulation of airports a simpler task. Many of the traditional tools of economic regulation are designed taking into account the incentives of profit-maximising monopolies. This means they are likely to be most effective when applied to privately owned airports. This sort of regulation may actually have an adverse effect where the airport is under public ownership, where the incentives are less obvious and where the focus may be on the wider benefits of the airport’s operations than purely on financial return.

Of course, increasing privatisation may also mean more airports than before have an incentive to exploit any market power they have in order to increase their profits. The Commission’s decision to review the Airport Charges Directive in 2016-17 is therefore timely. In the meantime, airlines should refrain from pressing the panic button, at least for now.

The ACI report offers up some reasons for this change in ownership. This includes the sale of airports to reduce pressure on public funds and a desire to increase efficiencies and expertise in the running of the airport. (We wonder whether similar pressures could soon be appearing in the air navigation service provider sector). For the ACI, the increasing privatisation of airports is purely a good news story, with upsides for everyone. It is also keen to attribute this trend to commercial pressures arising from increasing airport competition. Well they would, wouldn’t they?

There will be some worried airlines reading the report. After all, private investors will expect a decent return for their investment, and the increasing privatisation of the European airport industry is an indication that airports are providing a lucrative investment. Insert references to monopoly service providers here. Indeed, a report issued by A4E at the start of this year alleges that airport charges have increased by 80% at Europe’s largest 21 airports since 2005.

Before the airlines start banging at the doors of the European Commission demanding heavy-handed regulation (oops – too late), it is worth taking a step back and considering the consequences of the privatisation of European airports.

The first thing to consider is whether privatisation will have any impact on the extent to which there is competition between airports in Europe. Deducing this is no easy task. Both airlines and airports have entrenched views that are not always helpful when it comes to having a real discussion of the issues, while it can be a complex process to measure the ability of passengers and airlines to substitute between different airports.

It is worth considering that the relentless pursuit of profit associated with a private investment has the potential to encourage airports to adopt more innovative approaches to attracting passengers and airlines. In the case of some, this may include attracting customers away from other airports in the region.

Where there is evidence that an airport has market power, this does necessarily mean that its charges are too high or that there is a need for heavy-handed regulation. This applies even with a profit-motivated privatised airport. It is not market power that is the issue, it is the abuse of the market power.

As we discussed in a previous blog post, it may be in the airport’s commercial interests to set aeronautical charges at a level that makes it more attractive to airlines and increase the number of passengers using its facilities. Setting prescriptive pricing guidelines could stifle innovative pricing to the detriment of airlines, airports and ultimately passengers. Privatised airports, with their commercial focus, should be encouraged to challenge the traditional airport business model not buckle under it.

Meanwhile, much of the recent evidence suggests that light-handed regulation can act as a sufficient deterrent, particularly at airports with a strong commercial focus. The threat of further heavy-handed regulation can be enough to incentivise airports to behave in a way that does not antagonise the airlines, and therefore the regulator. After all, being subject to a price or revenue cap can take up a chunk of an airport’s (and an airline’s) resources and limits the airport’s ability to make commercial decisions. Airport regulators in the UK, Australia and New Zealand have all moved towards more light-handed regulatory approaches that, on the whole, have provided to be successful

Increasing privatisation may actually make the economic regulation of airports a simpler task. Many of the traditional tools of economic regulation are designed taking into account the incentives of profit-maximising monopolies. This means they are likely to be most effective when applied to privately owned airports. This sort of regulation may actually have an adverse effect where the airport is under public ownership, where the incentives are less obvious and where the focus may be on the wider benefits of the airport’s operations than purely on financial return.

Of course, increasing privatisation may also mean more airports than before have an incentive to exploit any market power they have in order to increase their profits. The Commission’s decision to review the Airport Charges Directive in 2016-17 is therefore timely. In the meantime, airlines should refrain from pressing the panic button, at least for now.